Sometimes, it’s not good to be King

By: Jason Blackwell, CFA, CAIA®, Chief Investment Strategist; Brian Katz, CFA, Chief Investment Officer & Richard Steinberg, CFA, Chief Market Strategist

When we look back on the returns of September 2019, there will be little hint that anything extraordinary happened. There were some changes in leadership but nothing out of the ordinary. Developed international and emerging market equities outperformed US stocks for the month; a welcome change from the last few years. Value stocks outperformed Growth globally as investors turned away from momentum driven names that have dominated the market. Bond yields rose modestly leading to modestly negative returns across most of the fixed income market, and the yield curve (as measured by the 2-year and 10-year Treasury bond) steepened back out of its August inversion. Underlying these returns, however, were some very significant headlines that reminded us that sometimes it’s not “good to be a king.”

In the last week of the month, President Donald Trump was accused of misusing his authority to pressure a foreign government to investigate a political rival; he now faces the most significant impeachment threat of his presidency. Within the same news cycle, British Prime Minister Boris Johnson was dealt a significant blow by the Supreme Court of the United Kingdom prompting calls for his resignation. In the very same week, one of the most highly anticipated IPOs of the year, The We Company (parent company of WeWork), was indefinitely delayed based on governance and valuation concerns. Its CEO and co-Founder, Adam Neumman, was subsequently removed from his post and lost his majority voting control of the company, although he remains Chairman. In conclusion, it was a bad week to be a leader.

The impact on the stock market from presidential impeachment proceedings is difficult to predict except to assume that it will cause an uptick in volatility. There (thankfully) is not much history for us to rely on.

- During the investigation of President Nixon, the market declined throughout the investigation, sold off sharply after the “Saturday Night Massacre,” and continued to fall after his resignation. However, this event coincided with a secular bear market as oil prices spiked, inflation rose sharply, and markets sold off from historically high valuations.

Source: Strategas Securities, LLC

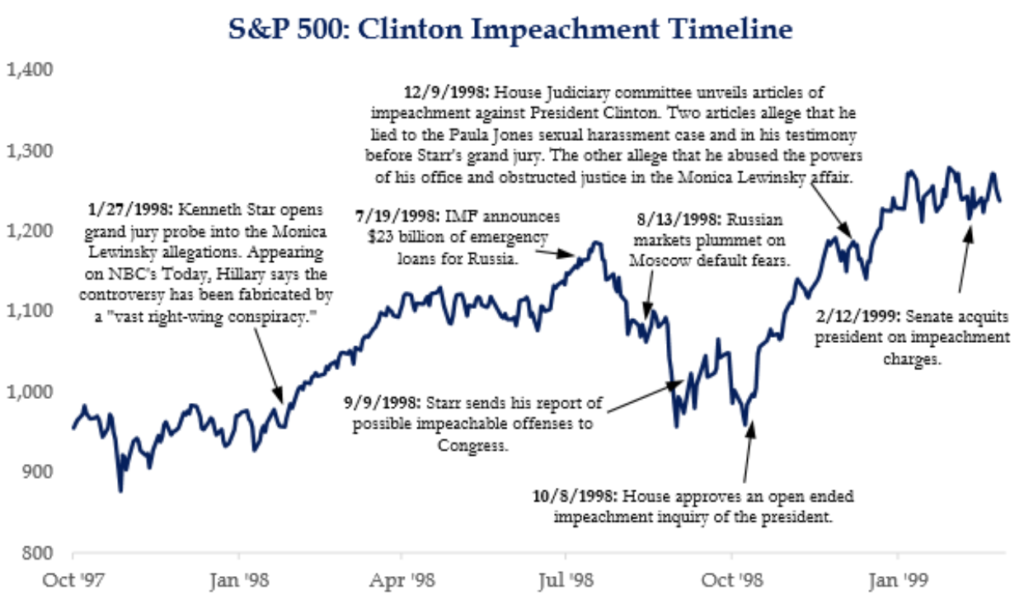

- In the case of President Clinton, markets sold off during the initial investigation but rallied strongly from the time of the official impeachment inquiry through his ultimate acquittal. Similarly, before drawing conclusions, we must understand the pre-existing market environment. Simultaneous to the investigation, the Russian debt crisis was in full swing, which sparked fears of global contagion.

Source: Strategas Securities, LLC

- In the current situation, the prevailing wisdom suggests that the President has a high probability of being impeached by the House and a low probability of being removed from office by the Senate. Broad concerns over the economy, specifically regarding US trade policies, are weighing on investor sentiment, however. Should the President be removed from office, it’s likely that Vice President Pence would continue many of the policies of the Trump Administration. While we expect that the impeachment news cycle over the coming months will exacerbate volatility in the market, we do not anticipate longer-term impacts from the political maneuvering.

The relationship between the UK and the EU appears likely to cause similar volatility. British Prime Minister Johnson is continuing to push for an October 31 break from the EU and has submitted new plans to try to reach an agreement. The adjustments to the withdrawal agreement have been met with stiff opposition. While Parliament has passed a law requiring that he seek an extension if a deal cannot be reached, there is increasing concern that Johnson will seek a loophole leaving the only remaining option for the opposition to avoid a no-deal Brexit coming from a no-confidence vote. That’s a risky proposition as Johnson’s Conservative party is ahead in the polls and there is no clear leader to take hold from the coalition of opposition parties; so risky in fact, that Johnson has invited the party to “back or sack” him.

- In the short run, we believe there is a greater probability that Brexit will be delayed again while the government determines the next course of action.

- Longer term, the ruling by the UK Supreme Court is potentially much more significant. The institution just celebrated its 10-year anniversary, and this was perhaps its boldest ruling to date. It is possible that this is the beginning of a new era in the UK with more checks and balances between the executive, legislative, and judicial branches.

- From a market perspective, the uncertainty will likely continue to weigh on equities as companies continue to “hope for the best but prepare for the worst” by slowing hiring and building up inventories. We remain generally constructive on European equities (and international more broadly) from a valuation perspective but would like to see more clarity in the political realm before we are willing to meaningfully increase exposure.

The disastrous near-IPO for The We Company has captured the attention of private equity investors. It was one of the most highly anticipated IPOs of the year with the most recent private round of financing valuing the company at an estimated $47 billion.

- In mid-August, the company filed its initial documents with the SEC to go public. The filing highlighted the firm’s exceptional revenue growth and offsetting spending. The filing further exposed governance failures by the board, including self-dealing with the CEO, which allowed him to cash out $700 million ahead of the IPO, and granting the wife authority that would supersede his successor in the event of his death.

- Investors understandably balked. By early September, the underwriter’s valuation had dropped to between $20-30 billion. By the end of September, Neumann resigned from the CEO position and lost his majority voting rights, and the IPO was delayed indefinitely.

- The story has been offered up by several commentators as a microcosm of the risks of private-equity-funded IPOs. While private equity does come with a number of risks, we believe that they can be managed through careful due diligence and ensuring alignment of interests.

We continue to see significant short- and medium-term risks on the horizon. If we have learned anything over the last ten years of risk-on/risk-off markets, it’s that the anticipation of news has a greater impact than the news itself. While the odds of removing the US president from office or the UK experiencing a painful no-deal Brexit appear to remain relatively low, they are likely to continue to move markets over the next 12-18 months.

October Update

While we do not typically comment on volatility that is measured in days rather than months (or even years), we do think it appropriate to mention the first few days of October as US markets sold off sharply on October 1stand 2ndwith the S&P losing 3.0%, eclipsing the modest gains of the 3rdquarter. The declines came as data on US manufacturing showed the second consecutive month of contraction in September and a report indicating a slowdown in hiring. The backbone of the US economy has been the consumer. In late September, The Conference Board’s Consumer Confidence Index of current conditions declined modestly; however, the future expectations component showed a steep decline. This data supports the view that a recession is coming at some point. We continue to believe that the best defense is to build diversified portfolios that are designed to withstand the ensuing volatility and allow our clients to stick to their long-term financial plans.